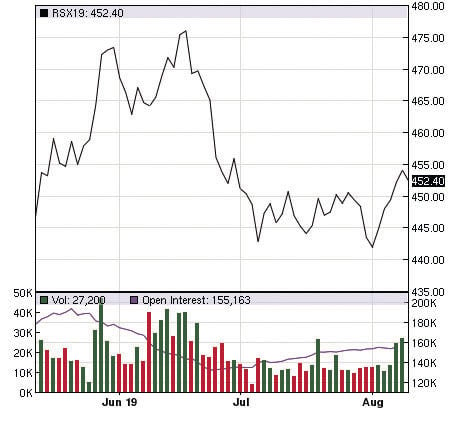

Local cash canola prices ranged from a low of $14.08 to a high of $14.60 per hundredweight on Aug. 7, which is down about $0.20 from two weeks ago, according to Barry Coleman, executive director of the Northern Canola Growers Association (NCGA). However, the futures market has shown little movement during this time and are at the same level as two weeks ago.

Cash canola prices continue to drift lower

1 of 2

Canola future price chart

Most Popular

The 2026 wheat crop got off to a rough start with delayed planting in some regions due to wet conditions, while other areas experienced drough…

The overall world durum situation for 2026 looks pretty promising with production forecast to potentially reach a record 1.43 billion bushels.…

The drop in crude oil prices has caused the price of canola to fall considerably in the past two weeks, following the lead of soybean oil. Can…

The uncertainties of the war with Iran and the turmoil it has caused in the world economy continues to impact grain commodity markets, includi…

The U.S. Department of Agriculture (USDA) came out with its latest supply and demand report in mid-June, a report which was considered neutral…