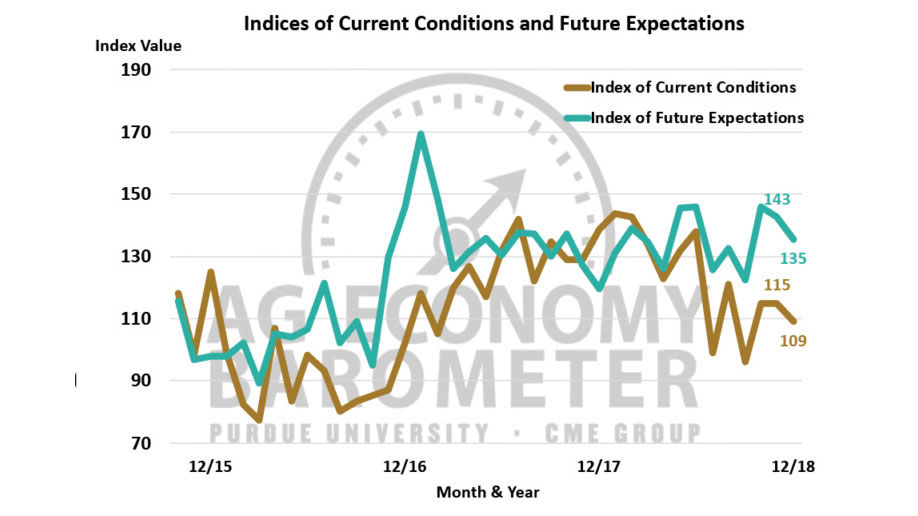

Editor’s note: The following was written by James Mintert and Michael Langemeier for the Purdue University/CME Group Ag Economy Barometer Jan. 8.

People are also reading…

E-edition PLUS unlimited articles & videos

Personalized news alerts with our mobile app

*FREE access to newspapers.com archives

Hundreds of games, puzzles & comics online

*Refers to the latest 2 years of agupdate.com stories. Cancel anytime.

Editor’s note: The following was written by James Mintert and Michael Langemeier for the Purdue University/CME Group Ag Economy Barometer Jan. 8.

Get local news delivered to your inbox!

Get up-to-the-minute news sent straight to your device.