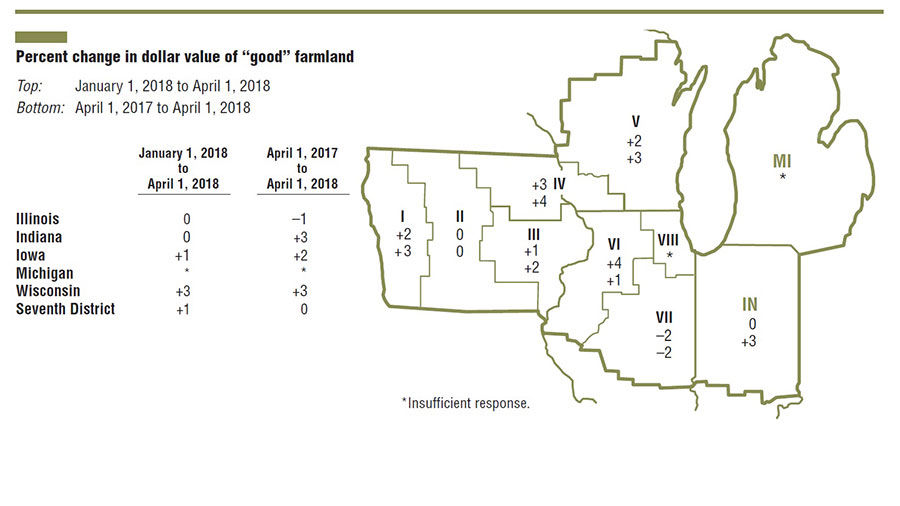

Editor’s note: The following was written by David B. Oppedahl, senior business economist at the Federal Reserve Bank of Chicago, for the May 2018 AgLetter.

People are also reading…

E-edition PLUS unlimited articles & videos

Personalized news alerts with our mobile app

*FREE access to newspapers.com archives

Hundreds of games, puzzles & comics online

*Refers to the latest 2 years of agupdate.com stories. Cancel anytime.

Editor’s note: The following was written by David B. Oppedahl, senior business economist at the Federal Reserve Bank of Chicago, for the May 2018 AgLetter.

Get local news delivered to your inbox!

Get up-to-the-minute news sent straight to your device.