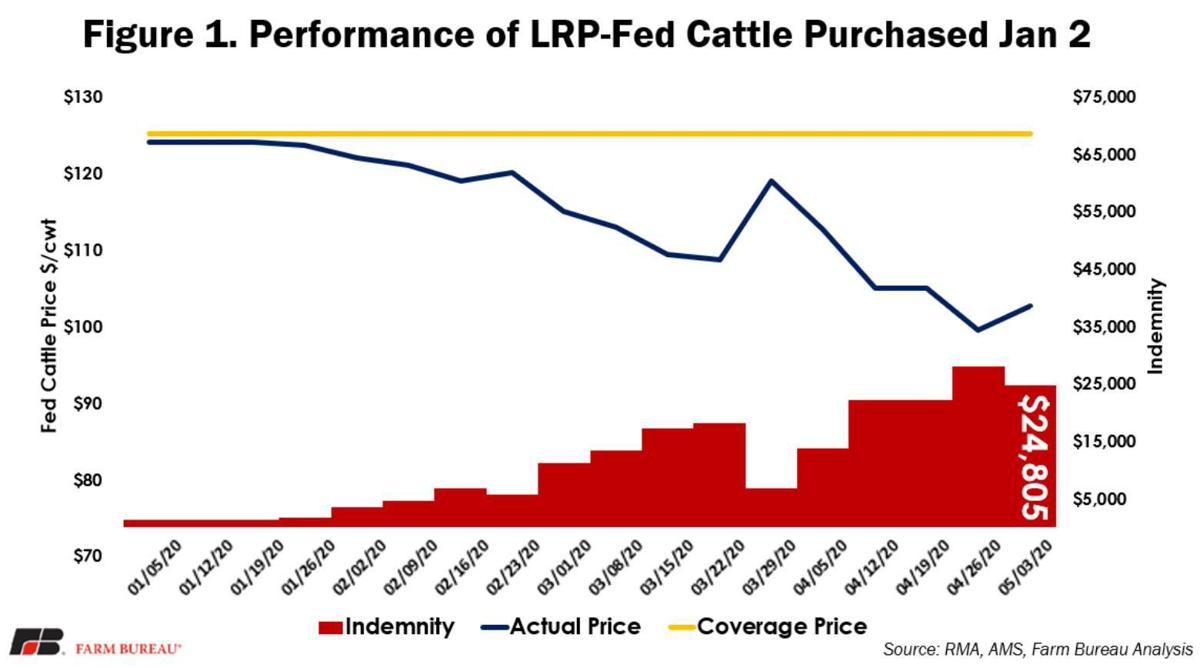

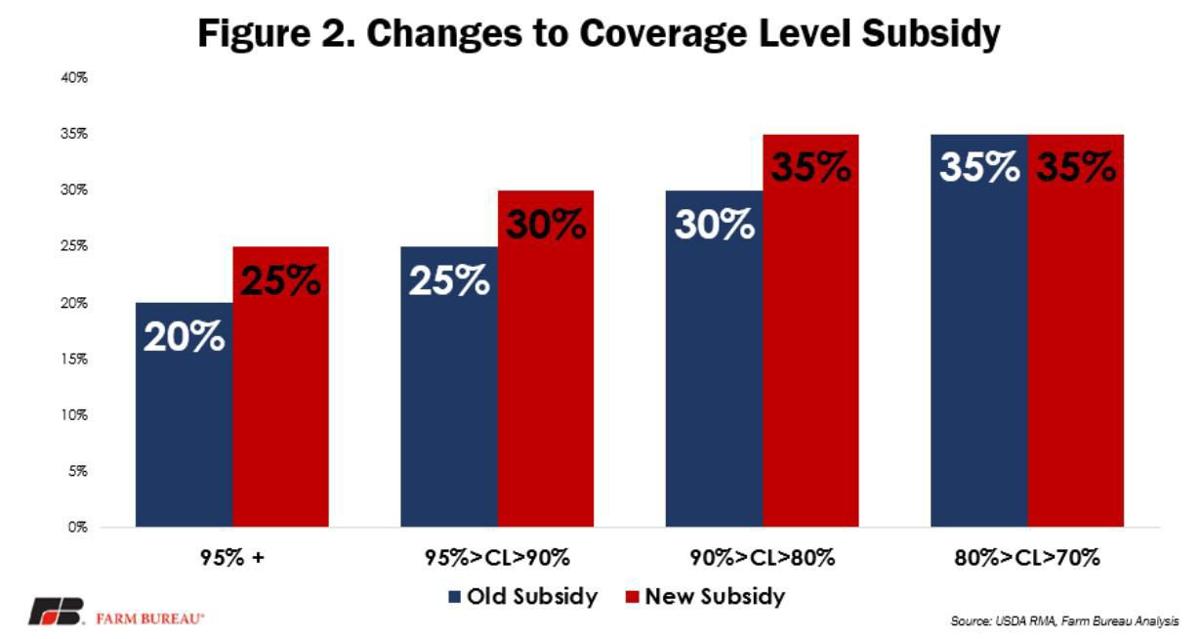

The U.S. Department of Agriculture’s Risk Management Agency announced June 9 that there are changes to the Livestock Risk Protection insurance program for swine, fed cattle and feeder cattle. The improvements, which include moving premium due dates and increasing premium subsidies, will be implemented by July 1 for the 2021 crop year. In addition to the changes, the Risk Management Agency is authorizing additional flexibilities – spurred by the coronavirus – for producers working with approved insurance providers.

USDA improves risk-management tool

1 of 2

The USDA's changes to Livestock Risk Protection insurance offer producers different premium-payment times and increased subsidies.